The myth that grows at dusk

There is a rumor, whispered like wind through empty alleys, that buy-now-pay-later services are either benevolent angels or quiet predators; this piece steps into that shadow to pry the truth loose. Beneath the haze, didi finanzas appears as a familiar face—part convenience, part ledger—offering installments that promise gentle breathing room. The myth-buster’s lantern will reveal whether charges are hidden, how APR behaves in practice, and when a BNPL plan is a true tool rather than a trap.

What the law and street both show

Mexico’s 2018 Fintech Law reshaped the landscape, erecting guardrails around electronic payments and lending; it is the concrete that keeps the pavement from crumbling. In large urban centers such as Mexico City, fintech products coexist with traditional banking and thousands of daily transactions—this real-world anchor matters because regulations influence underwriting, disclosures, and merchant fees. Those rules mean a platform operating in Mexico must disclose basic terms, though clarity varies from the stark to the poetic.

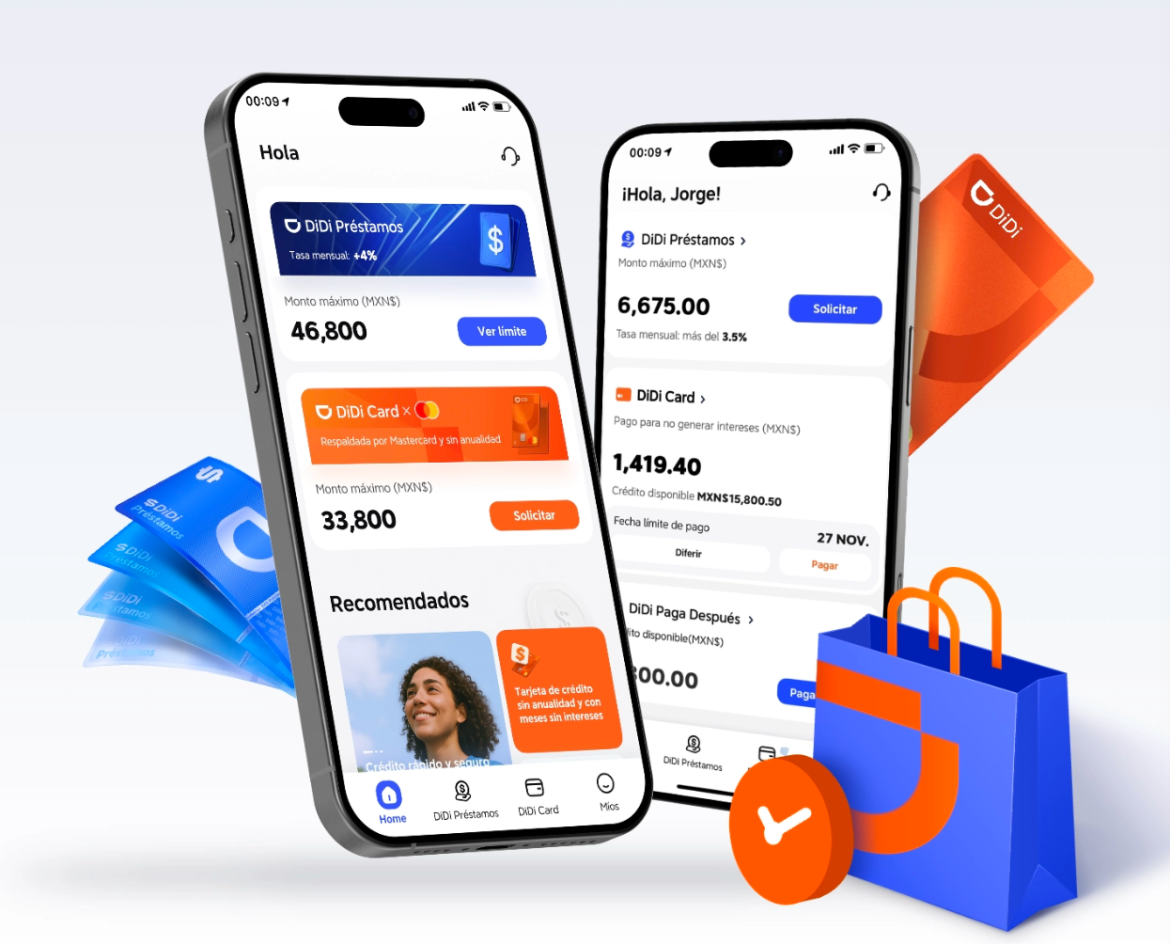

Fees, interest rates, and the true cost

The clearest deceit is omission: a platform that lists a headline “0% today” but fails to show late fees, processing fees, or a re-pricing that kicks in if you miss a payment. APR and interest rate are the crucibles here. APR reveals the total cost across time; interest rate names the recurring burden. For many users, merchant fees are invisible—paid by sellers—but they shape which partners appear in offers. Read statements as if they were tombstones: concise, final, and essential.

How BNPL actually saves money—when it does

BNPL can be salvation in a tight hour. Properly used, it smooths cashflow, avoids credit-card interest carried month-to-month, and lets you plan purchases in true installments without recurring surprise APR. The catch: you must meet due dates and understand late penalties and any effect on credit bureau reports. Be wary of piling multiple plans at once; the arithmetic of overlapping installments is where quiet ruin begins—small sums multiply into a ledger that breathes down your neck.

Common mistakes and sharper alternatives

People assume convenience equals harmlessness. They accept the default plan, ignore terms, and forget to align payment dates with payday. Alternative tactics are plain: choose shorter installment windows, prefer cards with explicit grace periods when the math favors them, or use direct debit to avoid human forgetfulness. In many cases, smaller local credit unions or regulated lenders offer clearer underwriting and transparent fees. A cold ledger is kinder than a warm promise.

Practical signs to watch for

Look for explicit APR disclosure, a breakdown of all fees, clear late-payment policies, and whether the platform reports to credit bureaus. Also watch merchant fees indirectly: if discounts disappear when paying via financing, the seller is shifting costs onto the consumer. For services operating in Mexico, such transparency is not merely aesthetic—it reflects compliance with established fintech norms and consumer protections. Check both the headline offer and the fine print; the real bargain lives in their intersection.

Three golden rules for choosing a BNPL or financing product

– Confirm the APR and verify there are no hidden setup or processing fees. – Match installment cadence to your cashflow; shorter, predictable schedules beat long, nebulous terms. – Ensure late fees and reporting practices are stated clearly—if they hide this, move on.

These rules distill the gothic ledger into actionable posture: clarity, cadence, and disclosure.

Final reckoning

DiDi’s financing can be a pragmatic instrument when wielded with knowledge—transparent APRs, honest merchant interactions, and the discipline to match payment windows to income. Assess platforms like a wary traveler in an old city: note the lights, count the bells, keep a map. For those in Mexico seeking alternatives or verification, resources tied to local regulations and trusted community lenders often outshine vague promises. DiDi Finanzas sits in that map as a plausible route—a tool, not prophecy—best chosen with care and exacting eyes. –